When Disaster Strikes: Understanding Individual Catastrophic Health Insurance

Why Individual Catastrophic Health Insurance Matters for Your Financial Protection

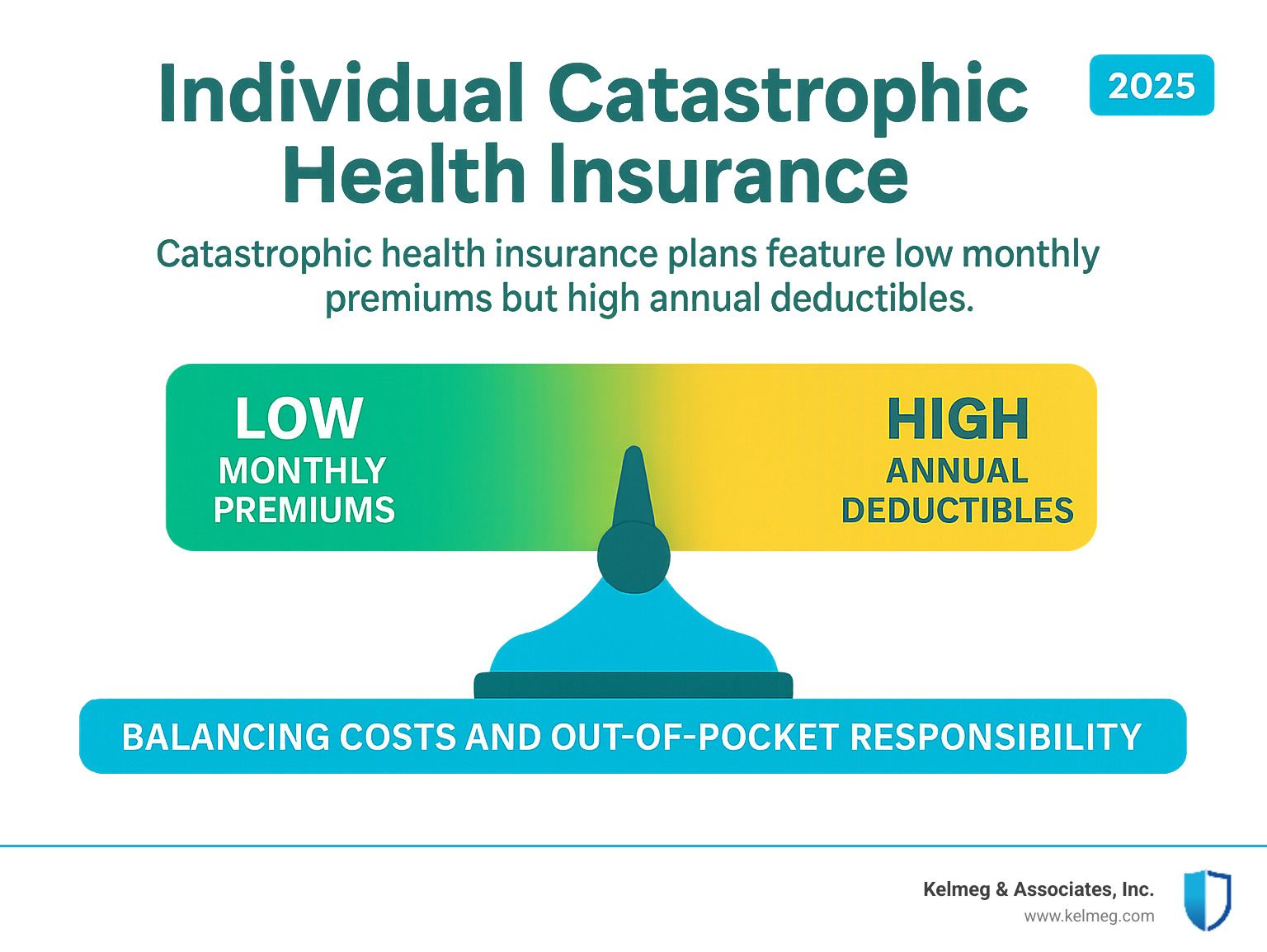

Medical emergencies can strike without warning, generating tens or even hundreds of thousands of dollars in medical bills that can lead to a devastating financial domino effect. For young adults or those facing significant financial hardship, traditional health insurance can seem unaffordably expensive, yet going without any coverage is a gamble with your financial future. This is where individual catastrophic health insurance offers a critical solution: a low-cost safety net specifically designed to protect you from the financial ruin of a worst-case medical scenario.

These Affordable Care Act (ACA)-compliant plans are not intended for routine healthcare but as a powerful form of financial protection against major medical events. They are defined by a unique structure:

- Low monthly premiums that are often the most affordable on the market.

- A very high annual deductible ($9,200 for an individual in 2025) that you must meet before most coverage begins.

- Strict eligibility rules, generally limiting plans to individuals under the age of 30 or those who have obtained a hardship or affordability exemption.

- Key pre-deductible benefits, including 100% coverage for preventive care and at least three primary care visits per year.

- No eligibility for government subsidies like premium tax credits, meaning you pay the full premium.

- 100% coverage for all in-network medical care after the high deductible has been met for the year.

This framework makes them an ideal choice for young, healthy individuals who can comfortably cover a high deductible from savings in an emergency but want absolute protection from financially devastating medical bills. As

Kelsey Mackley at Kelmeg & Associates, Inc., I specialize in helping clients steer the complexities of

individual catastrophic health insurance to determine if it truly aligns with their unique needs and financial situation. While not a fit for everyone, these plans can be an indispensable financial shield for the right person.

What Is Individual Catastrophic Health Insurance and How Does It Work?

Think of individual catastrophic health insurance as a financial shield built specifically for medical emergencies. It's a distinct type of health plan defined by the Affordable Care Act (ACA) that operates on a straightforward principle: you pay a very low monthly premium in exchange for taking on the majority of your initial medical costs yourself. The goal is to make basic financial protection accessible.

Here's the fundamental trade-off: you are responsible for all of your medical expenses out-of-pocket until you reach a very high annual deductible. For 2025, this deductible is set at

$9,200 for an individual, which also serves as your total out-of-pocket maximum for the year. To put this in perspective, a broken leg can cost over $7,500, and a three-day hospital stay can easily exceed $30,000. Once your spending on covered, in-network services hits that $9,200 threshold, the plan's protection fully engages, paying 100% of all your covered medical costs for the rest of the year. This structure is designed to protect you from the kind of six-figure bills from a serious accident or major surgery that could derail your financial future.

How Catastrophic Plans Differ from Other Health Plans

Catastrophic plans stand apart from other marketplace options (Bronze, Silver, Gold, Platinum) in several crucial ways:

- No Subsidies: This is the most significant difference. You cannot use premium tax credits or cost-sharing reductions with catastrophic plans. This is because the plans are already priced at a low point and are intended for a specific population not targeted by subsidies. This means you must pay the full monthly premium. For many individuals, a subsidized Bronze plan can actually be cheaper per month and offer better day-to-day benefits.

- Minimal Routine Care Coverage: Beyond the included preventive services and three annual primary care visits, you pay for almost all doctor visits, specialist appointments, and prescriptions out-of-pocket until your deductible is met. Bronze plans, while also having high deductibles, often offer more benefits like fixed copayments for generic drugs or specialist visits before the deductible is met, providing more predictable costs for routine care.

- Not the Same as Short-Term Insurance: It is vital to distinguish these two. Catastrophic plans are fully ACA-compliant, which means they must cover the 10 essential health benefits and cannot deny you coverage or charge you more based on pre-existing conditions. Short-term plans are not ACA-compliant, are not considered comprehensive coverage, and have significant limitations, often excluding pre-existing conditions and entire categories of care. For more on ACA options, see our guide to ACA Plans in Colorado.

Understanding the Costs: Premiums, Deductibles, and Out-of-Pocket Limits

With

individual catastrophic health insurance, your potential costs are clear and predictable. Your

monthly premium is low, but you are responsible for the full amount without any financial assistance. The

annual deductible is high - $9,200 in 2025, and set to rise to $10,600 in 2026. You pay 100% of your medical costs (except for the few pre-deductible benefits) until you reach this amount. The crucial protection comes from the

out-of-pocket maximum, which is the same as the deductible. Once you hit this limit with in-network, covered services, your financial responsibility for healthcare ends for the year. For official details on these limits, see the guidance from

CMS.

Who Is Eligible to Enroll in a Catastrophic Plan?

Not everyone can purchase

individual catastrophic health insurance. The Affordable Care Act (ACA) established strict eligibility rules to ensure these plans serve their intended audience: young, healthy individuals who do not expect to need significant medical care and those who genuinely cannot afford other types of coverage due to financial hardship.

The Age Requirement: For Individuals Under 30

If you are under the age of 30 when the plan year begins, you automatically qualify to purchase a catastrophic plan. No special application or exemption is needed. This rule acknowledges that, statistically, young adults are healthier and may prefer to pay a lower monthly premium in exchange for taking on more financial risk for day-to-day medical costs.

These plans are often a good strategic fit for:

- Healthy individuals who want the lowest possible monthly premiums while still having protection against major medical events.

- Students operating on a tight budget who need a reliable safety net.

- People between jobs or in other career transitions who need temporary, affordable coverage that is ACA-compliant.

It is crucial for anyone under 30 considering this path to have a separate emergency fund capable of covering the full deductible. Without accessible savings, a major medical event could still lead to significant debt, defeating the primary purpose of the insurance. Being under 30 gives you the flexibility to prioritize low monthly costs over comprehensive benefits, but this choice requires financial preparedness. To compare all your choices, see our guide on Individual Health Plans in Colorado.

Hardship and Affordability Exemptions for Those 30 and Over

Once you turn 30, your eligibility for a catastrophic plan changes. You can only enroll if you first apply for and receive an official exemption from the Health Insurance Marketplace. There are two main types of exemptions:

- Affordability Exemption: You may qualify for this exemption if the cheapest ACA-compliant plan available to you (typically a Bronze plan) would cost more than 7.28% of your Modified Adjusted Gross Income (MAGI) for 2025. This is designed for situations where standard insurance is officially deemed unaffordably expensive relative to your income.

- Hardship Exemption: This category covers a wide range of difficult life circumstances that make it challenging to purchase and afford standard health insurance. Common qualifying events include homelessness, eviction or foreclosure in the last 6 months, receiving a utility shut-off notice, death of a close family member, bankruptcy, substantial debt from medical expenses, or being a victim of domestic violence, fire, or a natural disaster.

To get an exemption, you must complete a specific application through the marketplace and provide supporting documentation. If your application is approved, you will receive an

Exemption Certificate Number (ECN), which you can then use to enroll in a catastrophic plan. The process requires extra steps and foresight, but it provides a vital option for those facing significant life and financial challenges. You can find more information on the

Hardship Exemption Application details page.

What Do Catastrophic Plans Cover?

Despite their name and low premiums,

individual catastrophic health insurance plans are not skimpy on the scope of what they cover. As fully ACA-compliant plans, they are legally required to cover the same 10 essential health benefits as all other Marketplace plans (Bronze, Silver, Gold, and Platinum). This comprehensive list includes everything from emergency services and hospitalization to prescription drugs, maternity and newborn care, and mental health and substance use disorder services. You can review the full requirements in the

Text of the Affordable Care Act defining benefits.

The key difference is not what is covered, but when the plan starts paying for those services. The coverage is structured in two distinct phases: before you meet your deductible and after.

Pre-Deductible Coverage: What You Get Before Meeting Your Deductible

Even before you meet the very high deductible, you receive some valuable benefits at no extra cost to you. These plans must provide:

- Preventive Care: 100% coverage for a wide range of preventive services when delivered by an in-network provider. This includes annual check-ups, immunizations like the flu shot, health screenings for blood pressure, cholesterol, and depression, certain cancer screenings, and counseling for topics like smoking cessation and healthy eating. For a full list, see the guide on Certain preventive health care.

- Three Primary Care Visits: You get at least three visits to your primary care physician (PCP) per year before the deductible applies. This is perfect for handling minor illnesses, managing a simple health concern, or conducting routine check-ups without having to pay the full cost out-of-pocket.

These pre-deductible benefits are designed to encourage you to maintain your health and catch potential issues early, which can help prevent a true medical catastrophe down the road.

Post-Deductible Coverage for Major Medical Events

Once your out-of-pocket spending on covered, in-network services reaches the high deductible (e.g., $9,200 in 2025), your

individual catastrophic health insurance plan transforms. It kicks in to cover 100% of all in-network medical costs for the remainder of the plan year. There is no coinsurance or additional copays for covered, in-network care. A critical aspect of this coverage is the plan's network. To receive the 100% coverage after meeting your deductible, you must use doctors, hospitals, and specialists that are 'in-network'. Going out-of-network can result in significantly higher costs, and those payments may not count toward your deductible or out-of-pocket maximum. Always verify that your preferred providers are in-network before enrolling.

This is where the plan's true value lies. For major medical events like a serious car accident, cancer treatment, or an unexpected surgery, medical bills can quickly exceed the deductible. After that point, all subsequent costs for hospitalization, treatments, and specialist care are fully covered, providing a firm and reliable ceiling on your financial liability. For families considering their options, our guide on Information on Family Insurance Plans in Colorado can offer additional context.

Is a Catastrophic Plan the Right Choice for You?

Deciding on

individual catastrophic health insurance requires an honest and thorough assessment of your health, your finances, and your personal tolerance for risk. It is an excellent and cost-effective fit for some individuals but can be a financially detrimental choice for others. For example, if you have chronic conditions that require regular doctor visits, specialist consultations, or ongoing prescriptions, you will likely spend far more out-of-pocket with a catastrophic plan than you would with a traditional plan, even one with a higher monthly premium.

Weighing the Pros and Cons of Individual Catastrophic Health Insurance

The main appeal of a catastrophic plan is its

very low monthly premiums. However, the most significant drawback is that you

cannot use premium tax credits or cost-sharing reductions. This is a critical factor, as a subsidized Bronze plan may actually cost an eligible person less per month while offering better day-to-day coverage. For many, the choice comes down to a catastrophic plan versus a Bronze plan. If you qualify for premium tax credits, a Bronze plan's monthly premium could be lower than a catastrophic plan's full price. Furthermore, many Bronze plans offer some cost-sharing for services like generic drugs or specialist visits before you meet your deductible, offering more day-to-day utility. The catastrophic plan's main advantage is the 100% coverage after the deductible, whereas a Bronze plan would still require you to pay coinsurance until you hit the separate out-of-pocket maximum. The protection against major expenses is another key pro: once you hit the deductible, you're 100% covered. The cons include the

very high deductible and the

strict eligibility rules.

| Feature | Individual Catastrophic Health Insurance | Bronze Plan |

|---|---|---|

| Monthly Premiums | Very Low (often the lowest available) | Higher than Catastrophic, but can be significantly reduced by premium tax credits for eligible individuals. |

| Annual Deductible | Very High (equals out-of-pocket maximum), e.g., $9,200 (2025) | High, but generally lower than Catastrophic plans (e.g., $6,000 - $8,000). |

| Out-of-Pocket Max | Highest allowed by ACA, e.g., $9,200 (2025) | High, but typically lower than Catastrophic plans. |

| Subsidy Eligibility | NO premium tax credits or cost-sharing reductions can be used. | YES, eligible for premium tax credits and, for some, cost-sharing reductions. |

| HSA Compatibility | Not currently (until 2026), as they are not considered HDHPs under current rules. | Some Bronze plans are High-Deductible Health Plans (HDHPs) and can be paired with an HSA. |

| Routine Care Before Deductible | Covers 3 primary care visits and all preventive services at no cost. | Varies by plan, but often offers more copay benefits for doctor visits or prescriptions before deductible is met. |

| Coverage After Deductible | 100% coverage for covered services. | Typically involves coinsurance (e.g., 20-50%) until the out-of-pocket maximum is reached. |

| Eligibility | Restricted to individuals under 30 or those with a hardship/affordability exemption. | Broadly available to anyone, regardless of age or hardship status. |

Catastrophic Plans and Health Savings Accounts (HSAs)

Currently, individual catastrophic health insurance plans are not compatible with Health Savings Accounts (HSAs). This is a significant disadvantage, as it means you miss out on the powerful triple tax advantage of using an HSA to save and pay for medical expenses. The reason for this incompatibility is that their specific structure does not meet the IRS definition of a High-Deductible Health Plan (HDHP). However, this is set to change: starting in 2026, new legislation will allow catastrophic plans to be HSA-eligible, making them a much more attractive option for combining low premiums with tax-advantaged savings. For more on options for freelancers, see our guide on Health Insurance For Self Employed in Colorado.

When a Catastrophic Plan Might Not Be Enough

A catastrophic plan is generally a poor fit if you have:

- Chronic conditions like diabetes, asthma, or heart disease that require ongoing care and medication.

- Frequent doctor visits beyond the three covered primary care appointments.

- Regular prescriptions, as you'll pay the full, negotiated cost until the high deductible is met.

- Young children, who often need unpredictable and frequent medical care for illnesses and injuries.

Most importantly, if you are a low-income individual eligible for subsidies, a Bronze or Silver plan is almost always a better financial choice. The subsidies can make these plans more affordable on a monthly basis and far more comprehensive in their day-to-day coverage. Learn more at Low Income Health Insurance In Colorado.

How to Apply for a Plan or Exemption

Applying for individual catastrophic health insurance is a straightforward process, but timing and eligibility are key. Most people must enroll during the annual ACA Open Enrollment period, which typically runs from November 1 to December 15 for coverage starting January 1 of the next year. If you miss this window, you may still be able to enroll during a Special Enrollment Period (SEP) if you experience a qualifying life event. Common SEP triggers include loss of other health coverage (like from a job), marriage, divorce, having a baby, adopting a child, or moving to a new zip code where your old plan is not available.

The application process for all Marketplace plans, including catastrophic ones, begins at the Official Healthcare.gov site or your state's specific marketplace exchange.

Enrolling in an Individual Catastrophic Health Insurance Plan

If you are under 30, the process is simple and does not require any pre-approval:

- Visit Healthcare.gov and create an account or log in to your existing one.

- Complete the application with your personal, household, and income information. Be prepared with Social Security numbers, income information (like pay stubs or W-2s), and details about any employer-offered insurance for everyone in your household.

- The system will show you all the plans you are eligible for. Compare the available plans. Catastrophic plans will be listed alongside the metal-tier options (Bronze, Silver, Gold).

- Select your desired catastrophic plan and complete the enrollment process.

- Make your first premium payment directly to the insurance company to activate your coverage.

Because your age is the only primary requirement, you will not need any special exemptions or additional paperwork.

The Process for Obtaining a Hardship or Affordability Exemption

If you are 30 or older, you must first obtain an exemption before you are allowed to enroll in a catastrophic plan. This process requires more steps and should be started well in advance of when you need coverage:

- Determine Your Eligibility: First, carefully review the criteria to decide if you qualify for an affordability exemption (based on a specific income calculation) or a hardship exemption (based on specific life circumstances).

- Complete the Application: Fill out the correct exemption application form, which can be found on Healthcare.gov.

- Gather Documentation: Collect the necessary documents to prove your eligibility. This could include income statements for an affordability exemption or eviction notices, bankruptcy filings, or other proof for a hardship exemption.

- Submit Your Application: Send the completed form and all supporting documentation to the Health Insurance Marketplace as instructed.

- Receive Your ECN: If your application is approved, you will receive an Exemption Certificate Number (ECN). This process can take several weeks, so it is critical to apply early.

- Enroll in a Plan: With your ECN, you can return to the marketplace to shop for and enroll in an available catastrophic plan before the enrollment deadline.

For detailed instructions, refer to the official

form for obtaining an exemption. Navigating this process can be complex, and at Kelmeg & Associates, Inc., we can guide Colorado residents through these steps at no cost to ensure it is done correctly.

Frequently Asked Questions about Catastrophic Coverage

Because

individual catastrophic health insurance works so differently from more traditional health plans, many important questions arise. Here are clear, concise answers to the most common ones.

Can I use premium tax credits or other subsidies with a catastrophic plan?

No. This is a firm rule. Catastrophic plans are not eligible for any form of government subsidy available through the ACA Marketplace. You cannot use premium tax credits (which lower your monthly payments) or cost-sharing reductions (which lower your deductibles, copays, and coinsurance). You must pay the full, unsubsidized premium yourself. Because of this rule, an individual who is eligible for subsidies will often find that a subsidized Bronze or Silver plan is cheaper per month and offers more robust coverage.

Are catastrophic plans compatible with a Health Savings Account (HSA)?

Not yet, but soon. Currently, catastrophic plans do not meet the specific requirements set by the IRS to be considered a High-Deductible Health Plan (HDHP), which is a prerequisite for being paired with an HSA. This means you miss out on the significant tax advantages of contributing to and using an HSA. However, this is changing: new federal rules mean that

starting in 2026, catastrophic plans will become HSA-eligible, which will make them a much more powerful financial tool for saving for medical expenses.

What happens if I have a catastrophic plan but need regular, non-emergency medical care?

You will pay for most of it out of your own pocket until you meet your high annual deductible. Your plan does provide some key benefits before the deductible is met, which include:

- Three primary care visits per year.

- Free preventive care, including annual physicals, various health screenings, and immunizations.

For anything else, such as specialist visits, urgent care appointments, physical therapy, or most prescription medications, you will be responsible for paying the full, insurer-negotiated rate until your total spending on these services reaches the annual deductible. Once you meet that deductible, your plan pays 100% of covered in-network costs for the rest of the year. These plans are truly designed for major medical events, not for managing routine or ongoing healthcare needs.

What happens if my income changes and I become eligible for subsidies mid-year?

If you have a catastrophic plan and your income drops significantly, you may be able to switch to a subsidized plan like a Bronze or Silver plan. A change in income that makes you newly eligible for premium tax credits is often considered a qualifying life event that opens a Special Enrollment Period. You would need to report your income change to the Marketplace as soon as possible. The system will then determine your eligibility for subsidies and allow you to see your new options and enroll in a different plan that may offer better coverage for a lower monthly cost.

Conclusion

Individual catastrophic health insurance is a specialized product designed for a very specific purpose: to provide a reliable financial safety net against worst-case medical scenarios at the lowest possible monthly cost. It operates on an all-or-nothing principle - you handle routine costs yourself in exchange for 100% coverage after a major medical event pushes you past the high deductible.

These plans are not a one-size-fits-all solution. The strict eligibility rules - being under 30 or qualifying for a hardship exemption - ensure they are used by those who are either very healthy or facing significant financial challenges. While they cover all essential health benefits required by the ACA, the lack of subsidy eligibility and the high out-of-pocket threshold make them impractical and often more expensive for anyone with chronic conditions or regular healthcare needs.

The decision hinges on a clear-eyed assessment of your personal situation. If you are young, in excellent health, have a robust emergency fund ready to cover the high deductible, and are not eligible for significant subsidies, a catastrophic plan can be a smart, cost-effective way to secure essential financial protection. However, if you anticipate needing medical care, have chronic conditions, or if subsidies make other plans more affordable, a Bronze or Silver plan will almost certainly be a better value. The upcoming HSA compatibility in 2026 will make these plans even more appealing for their target demographic.

Choosing a health plan is a deeply personal decision based on your health, finances, and risk tolerance.

Individual catastrophic health insurance is not inherently good or bad - it is about whether it is the right fit for you. For residents of Colorado, Kelmeg & Associates, Inc. can provide expert, no-cost guidance to help you compare all your options and find the right protection for your peace of mind. Explore your choices by visiting our page on

Individual Health Insurance Plans in Colorado.